As thousands of restaurants, hotels, and local businesses in the U.S. struggle to stay open, delinquency rates across commercial mortgage-backed securities (CMBS)—fixed income investments backed by a pool of commercial mortgages— have tripled in three months to 10.32%. In just a few months, delinquency rates have already effectively reached their 2012 peaks. To put this in perspective, consider that it took well over two years for mortgage delinquency rates to reach the same historic levels in the aftermath of the housing crisis of 2009. The above chart draws data from Trepp and illustrates the recent shocks to the CMBS market, broken down by property type.

Storm Rumblings

While there is optimism in some areas of the market, accommodation mortgages have witnessed delinquency rates soar over 24%. Amid strict containment efforts in April, average revenues per room plummeted all the way to $16 per night—an 84% drop. Similarly, retail properties have been rattled. Almost one-fifth are in delinquencies. From January-June 2020, at least 15 major retailers have filed for bankruptcy and over $20 billion in CMBS loans have exposure to flailing chains such as JCPenney, Neiman Marcus, and Macy’s. On the other hand, industrial property types have remained stable, hovering close to their January levels. This is likely attributable in part to the fact that the rise in e-commerce sales have helped support warehouse operations. For multifamily and office buildings, Washington’s stimulus packages have helped renters to continue making payments thus far. Still, as the government considers ending stimulus packages in the near future, a lack of relief funding could spell trouble.

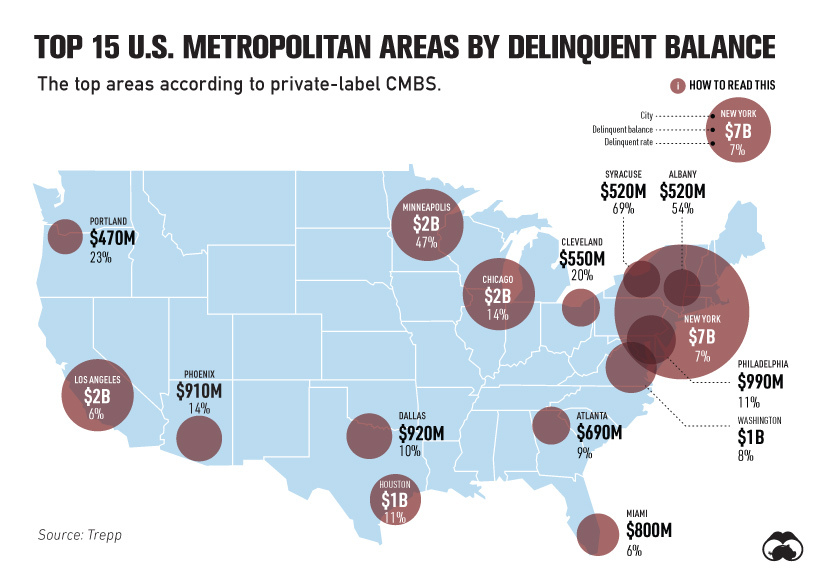

Weighing the Impact on U.S. Cities

How do delinquency rates vary across the top metropolitan areas in America? Below, we can see that the delinquent balance and delinquency rates vary widely by city. Note that this data is for private-labeled CMBS, which are issued by investment banks and private entities rather than government agencies.

Despite the New York city metropolitan area having a delinquent balance of $7 billion, its delinquency rates fall on the lower end of the spectrum, at 7%. New York alone accounts for 18% of the total balance of private-label CMBS. By comparison, the Syracuse metropolitan area has an eye-opening delinquency rate of 69%. Syracuse is home to the shopping complex, Destiny USA, which is facing tenant uncertainties due to COVID-19. The six-story mall attracts 26 million visitors annually. Like the overall market, delinquencies are being driven by accommodation and retail properties across many of these U.S. metropolitan areas.

What Comes Next

What happens when delinquency rates get too high? Often, when borrowers do not make payment after a reasonable amount of time, they enter into default. While time ranges can vary, defaults typically take place after at least 60 days of nonpayment. Between May and June, defaults in the CMBS market surged 792% to $5.5 billion. As effects reverberate, properties could eventually fall into foreclosure. At the same time, institutional investors who own these types of securities, which include pensions, could begin seeing steep losses. That said, the Federal Reserve has set up mechanisms to purchase CMBS loans with the highest credit quality. This is designed to inject liquidity into the mortgage market, while also financing small and mid-sized properties that house small businesses. In turn, this can enable the employment of millions of Americans. Of course, it remains to be seen whether the mortgage market will face a sustained downturn akin to the financial crisis, or if the temporary decline will soon subside. on Last year, stock and bond returns tumbled after the Federal Reserve hiked interest rates at the fastest speed in 40 years. It was the first time in decades that both asset classes posted negative annual investment returns in tandem. Over four decades, this has happened 2.4% of the time across any 12-month rolling period. To look at how various stock and bond asset allocations have performed over history—and their broader correlations—the above graphic charts their best, worst, and average returns, using data from Vanguard.

How Has Asset Allocation Impacted Returns?

Based on data between 1926 and 2019, the table below looks at the spectrum of market returns of different asset allocations:

We can see that a portfolio made entirely of stocks returned 10.3% on average, the highest across all asset allocations. Of course, this came with wider return variance, hitting an annual low of -43% and a high of 54%.

A traditional 60/40 portfolio—which has lost its luster in recent years as low interest rates have led to lower bond returns—saw an average historical return of 8.8%. As interest rates have climbed in recent years, this may widen its appeal once again as bond returns may rise.

Meanwhile, a 100% bond portfolio averaged 5.3% in annual returns over the period. Bonds typically serve as a hedge against portfolio losses thanks to their typically negative historical correlation to stocks.

A Closer Look at Historical Correlations

To understand how 2022 was an outlier in terms of asset correlations we can look at the graphic below:

The last time stocks and bonds moved together in a negative direction was in 1969. At the time, inflation was accelerating and the Fed was hiking interest rates to cool rising costs. In fact, historically, when inflation surges, stocks and bonds have often moved in similar directions. Underscoring this divergence is real interest rate volatility. When real interest rates are a driving force in the market, as we have seen in the last year, it hurts both stock and bond returns. This is because higher interest rates can reduce the future cash flows of these investments. Adding another layer is the level of risk appetite among investors. When the economic outlook is uncertain and interest rate volatility is high, investors are more likely to take risk off their portfolios and demand higher returns for taking on higher risk. This can push down equity and bond prices. On the other hand, if the economic outlook is positive, investors may be willing to take on more risk, in turn potentially boosting equity prices.

Current Investment Returns in Context

Today, financial markets are seeing sharp swings as the ripple effects of higher interest rates are sinking in. For investors, historical data provides insight on long-term asset allocation trends. Over the last century, cycles of high interest rates have come and gone. Both equity and bond investment returns have been resilient for investors who stay the course.