As global inequality continues to rise, how can wealth building tools become more accessible to the rest of the global population? Luckily, technological developments and their rapid adoption make this the right time for a new decentralized financial system to emerge:

The Internet: 3.9 billion users by the end of 2018 The proliferation of smartphones: Two-thirds of the unbanked have mobile phones Digital banking: over 2 billion users by end of 2018 Bitcoin and Blockchain: the emergence of new public blockchains

Today’s infographic comes to us from investment app Abra, and it highlights how public blockchains could help to enable a decentralized finance system.

What is Decentralized Finance?

Decentralized finance describes a new decentralized financial system that is built on public blockchains like Bitcoin and Ethereum. After all, Bitcoin and Ethereum aren’t just digital currencies — they’re foundational open source networks that could be used to change how the global economy works. There are six primary features that differentiate public blockchains from the private networks used by governments and traditional financial institutions:

Permissionless: Anyone in the world can connect to the network Decentralized: Records are kept simultaneously across thousands of computers Trustless: A central party isn’t required to ensure transactions are valid Transparent: All transactions are publicly auditable Censorship Resistant: A central party cannot invalidate user transactions Programmable: Developers can program business logic into low-cost financial services

In such a financial system, users will have access to apps that use public blockchains to participate in new open global markets – but how would this shape the global financial system for the better?

The Potential Impact of Decentralized Finance

Here are five ways that decentralized finance will have an impact on the world:

- Wider Global Access to Financial Services With decentralized finance, anyone with an internet connection and a smartphone could access financial services. There are a variety of barriers that prevent access in the current system:

Status: Lack of citizenship, documentation, credentials, etc. Wealth: High entry-level funds required to access financial services Location: Vast distance from functioning economies and financial service providers

In a decentralized financial system, a top trader at a financial firm would have the same level of access as a farmer in a remote region of India. 2. Affordable Cross-Border Payments Decentralized finance removes costly intermediaries to make remittance services more affordable for the global population. In the current system, it’s prohibitively expensive for people to send money across borders: the average global remittance fee is 7%. Through decentralized financial services, remittance fees could be below 3%. 3. Improved Privacy and Security In decentralized finance, users have custody of their wealth and can transact securely without validation from a central party. Meanwhile, in the current system, custodial institutions put people’s wealth and information at risk if they fail to secure it. 4. Censorship-Resistant Transactions In a decentralized financial system, transactions are immutable and blockchains can’t be shut off by central institutions like governments, central banks, or big corporations. In places with poor governance and authoritarianism, users can divest to the decentralized financial system to protect their wealth. For example, Venezuelans are already adopting Bitcoin to protect their wealth from government manipulation and hyperinflation. 5. Simple Use Plug and play apps will allow people to intuitively use decentralized financial services without the complexity of the centralized system. With a decentralized system, a woman in the Philippines could receive a loan from the U.S., invest in a business in Colombia, and then pay off her debt and purchase a home – all through interoperable apps.

The Potential Blue Sky

Unless governments and central banks suddenly cease to exist, it’s difficult to imagine a world where decentralized finance completely replaces their centralized counterparts. But what if they can co-exist? Public blockchains can interact with the traditional financial system to create a new hybrid model:

Users could conduct economic activity on public blockchains and exchange their new wealth into the centralized system. Users could hedge against systemic risk by diversifying their wealth holdings in both the central and decentralized system.

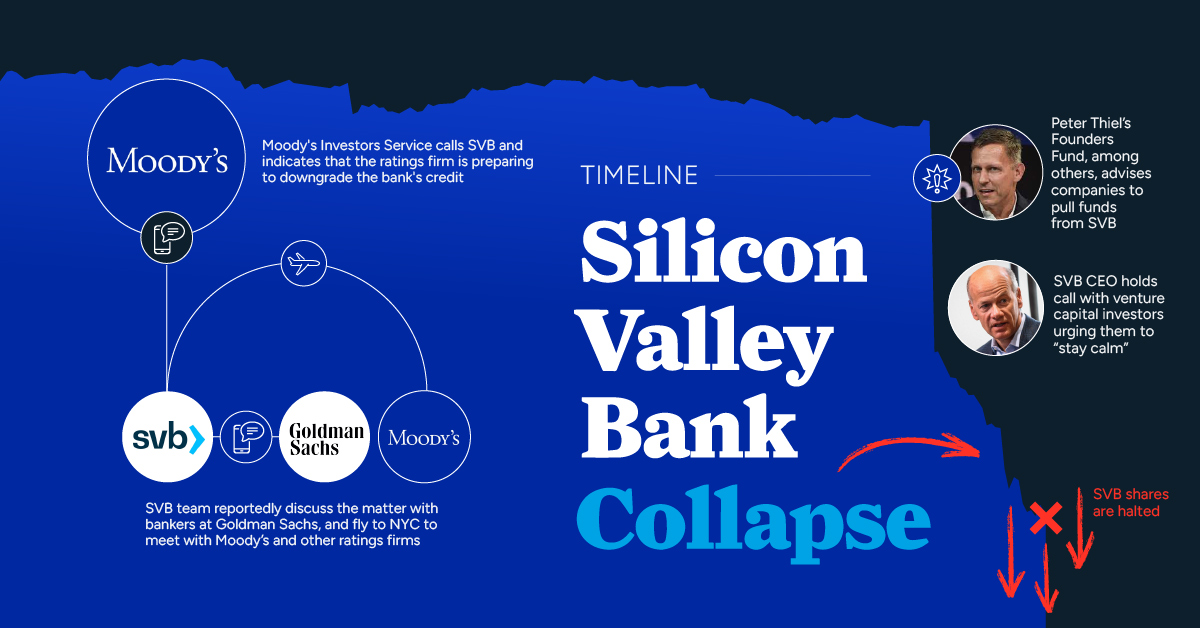

Like the internet with knowledge, decentralized finance could help democratize the financial system. But will we allow it? on But fast forward to the end of last week, and SVB was shuttered by regulators after a panic-induced bank run. So, how exactly did this happen? We dig in below.

Road to a Bank Run

SVB and its customers generally thrived during the low interest rate era, but as rates rose, SVB found itself more exposed to risk than a typical bank. Even so, at the end of 2022, the bank’s balance sheet showed no cause for alarm.

As well, the bank was viewed positively in a number of places. Most Wall Street analyst ratings were overwhelmingly positive on the bank’s stock, and Forbes had just added the bank to its Financial All-Stars list. Outward signs of trouble emerged on Wednesday, March 8th, when SVB surprised investors with news that the bank needed to raise more than $2 billion to shore up its balance sheet. The reaction from prominent venture capitalists was not positive, with Coatue Management, Union Square Ventures, and Peter Thiel’s Founders Fund moving to limit exposure to the 40-year-old bank. The influence of these firms is believed to have added fuel to the fire, and a bank run ensued. Also influencing decision making was the fact that SVB had the highest percentage of uninsured domestic deposits of all big banks. These totaled nearly $152 billion, or about 97% of all deposits. By the end of the day, customers had tried to withdraw $42 billion in deposits.

What Triggered the SVB Collapse?

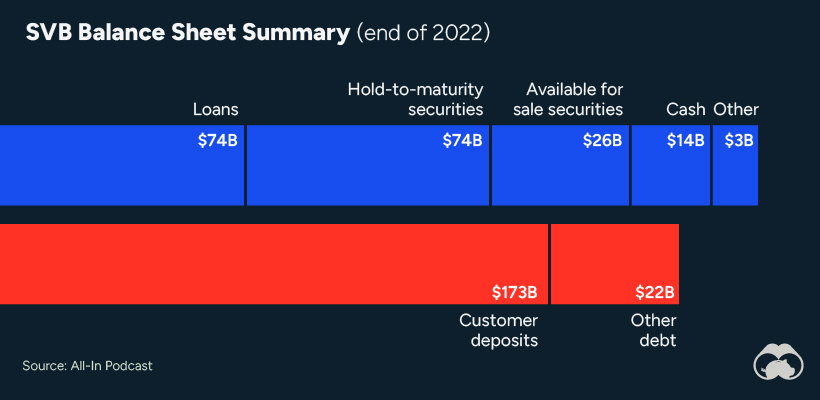

While the collapse of SVB took place over the course of 44 hours, its roots trace back to the early pandemic years. In 2021, U.S. venture capital-backed companies raised a record $330 billion—double the amount seen in 2020. At the time, interest rates were at rock-bottom levels to help buoy the economy. Matt Levine sums up the situation well: “When interest rates are low everywhere, a dollar in 20 years is about as good as a dollar today, so a startup whose business model is “we will lose money for a decade building artificial intelligence, and then rake in lots of money in the far future” sounds pretty good. When interest rates are higher, a dollar today is better than a dollar tomorrow, so investors want cash flows. When interest rates were low for a long time, and suddenly become high, all the money that was rushing to your customers is suddenly cut off.” Source: Pitchbook Why is this important? During this time, SVB received billions of dollars from these venture-backed clients. In one year alone, their deposits increased 100%. They took these funds and invested them in longer-term bonds. As a result, this created a dangerous trap as the company expected rates would remain low. During this time, SVB invested in bonds at the top of the market. As interest rates rose higher and bond prices declined, SVB started taking major losses on their long-term bond holdings.

Losses Fueling a Liquidity Crunch

When SVB reported its fourth quarter results in early 2023, Moody’s Investor Service, a credit rating agency took notice. In early March, it said that SVB was at high risk for a downgrade due to its significant unrealized losses. In response, SVB looked to sell $2 billion of its investments at a loss to help boost liquidity for its struggling balance sheet. Soon, more hedge funds and venture investors realized SVB could be on thin ice. Depositors withdrew funds in droves, spurring a liquidity squeeze and prompting California regulators and the FDIC to step in and shut down the bank.

What Happens Now?

While much of SVB’s activity was focused on the tech sector, the bank’s shocking collapse has rattled a financial sector that is already on edge.

The four biggest U.S. banks lost a combined $52 billion the day before the SVB collapse. On Friday, other banking stocks saw double-digit drops, including Signature Bank (-23%), First Republic (-15%), and Silvergate Capital (-11%).

Source: Morningstar Direct. *Represents March 9 data, trading halted on March 10.

When the dust settles, it’s hard to predict the ripple effects that will emerge from this dramatic event. For investors, the Secretary of the Treasury Janet Yellen announced confidence in the banking system remaining resilient, noting that regulators have the proper tools in response to the issue.

But others have seen trouble brewing as far back as 2020 (or earlier) when commercial banking assets were skyrocketing and banks were buying bonds when rates were low.