Battery minerals are set to become the new oil, with lithium-ion battery supply chains becoming the new pipelines. China is currently leading this lithium-ion battery revolution—leaving the U.S. dependent on its economic rival. However, the harsh lessons of the 1970-80s oil crises have increased pressure on the U.S. to develop its own domestic energy supply chain and gain access to key battery metals.

Introducing the New Energy Era

Today’s infographic from Standard Lithium explores the current energy landscape and America’s position in the new energy era.

An Energy Dependence Problem

Energy dependence is the degree of a nation’s reliance on imported energy, resulting from an insufficient domestic supply. Oil crises in the 1970-80s revealed America’s reliance on foreign produced oil, especially from the Middle East. The U.S. economy ground to a halt when gas prices soared during the 1973 oil crisis—altering consumer behavior and energy policy for generations. In the aftermath of the crisis, the government imposed national speed limits to conserve oil, and also demanded cheaper, smaller, and more fuel-efficient cars. U.S. administrations set an objective to wean America off foreign oil through “energy independence”—the ability to meet the country’s fuel needs using domestic resources.

Lessons Learned?

Spurred by technological breakthroughs such as hydraulic fracking, the U.S. now has the capacity to respond to high oil prices by ramping up domestic production. By the end of 2019, total U.S. oil production could rise to 17.4 million barrels a day. At that level, American net imports of petroleum could fall in December 2019 to 320,000 barrels a day, the lowest since 1949. In fact, the successful development of America’s shale fields is a key reason why the Organization of the Petroleum Exporting Countries (OPEC) has lost the majority of its influence over the supply and price of oil.

A Renewable Future: Turning the Ship

The increasing scarcity of economic oil and gas fields, combined with the negative environmental impacts of oil and the declining costs of renewable power, are creating a new energy supply and demand dynamic.

Oil demand could drop by 16.5 million barrels per day. Oil producers could face significant losses, with $380 billion of above-ground investments becoming worthless if the oil industry and oil-rich nations are not prepared for a surge in green energy by 2030.

Energy companies are hedging their risk with increased investment in renewables. The world’s top 24 publicly-listed oil companies spent on average 1.3% of their total budgets on low carbon technology in 2018, amounting to $260 billion. That is double the 0.68% the same group had invested on average through the period of 2010 and 2017.

The New Geopolitics of Energy: Battery Minerals

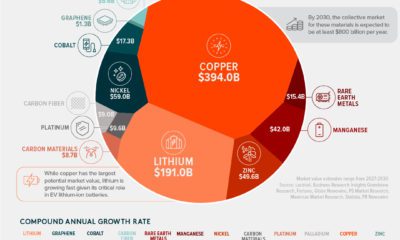

Low carbon technologies for the new energy era are also creating a demand for specific materials and new supply chains that can procure them. Renewable and low carbon technology will be mineral intensive, requiring many metals such as lithium, cobalt, graphite and nickel. These are key raw materials, and demand will only grow.

The cost of these materials is the largest factor in battery technology, and will determine whether battery supply chains succeed or fail. China currently dominates the lithium-ion battery supply chain, and could continue to do so. This leaves the U.S. dependent on China as we venture into this new era. Could history repeat itself?

The Battery Metals Race

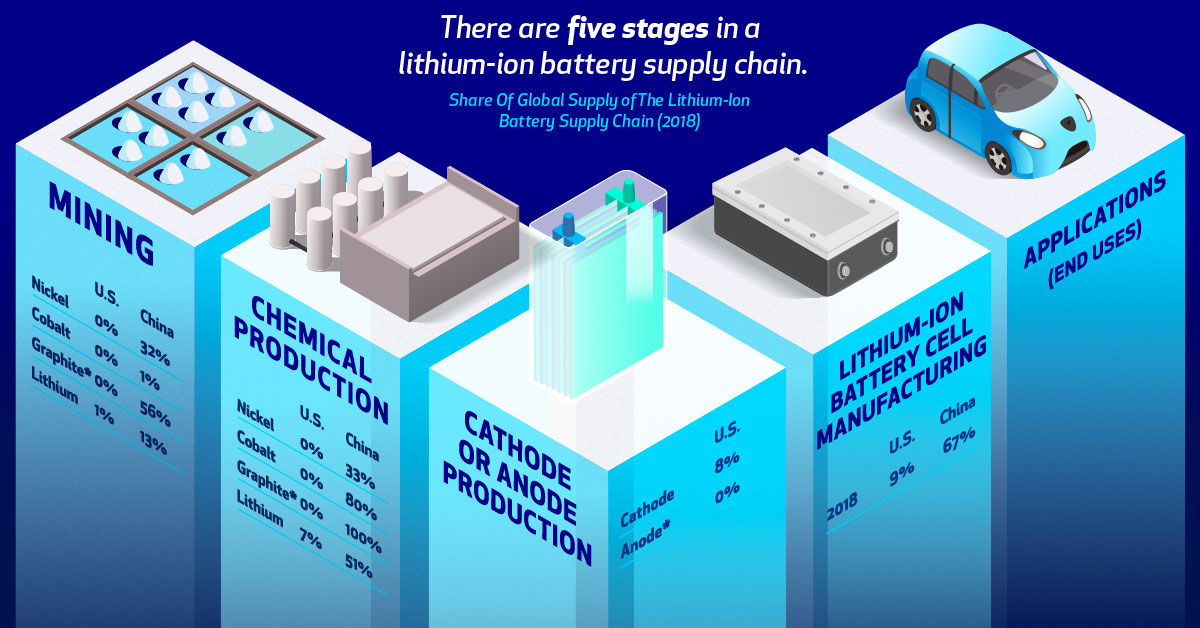

There are five stages in a lithium-ion battery supply chain—and the U.S. holds a smaller percentage of the global supply chain than China at nearly every stage.

China’s dominance of the global battery supply chain creates a competitive advantage that the U.S. has no choice but to rely on. However, this can still be prevented if the United States moves fast. From natural resources, human capital and the technology, the U.S. can build its own domestic supply.

Building the U.S. Battery Supply Chain

The U.S. relies heavily on imports of several keys materials necessary for a lithium-ion battery supply chain.

But the U.S. is making strides to secure its place in the new energy era. The American Minerals Security Act seeks to identify the resources necessary to secure America’s mineral independence. The government has also released a list of 35 minerals it deems critical to the national interest.

Declaring U.S. Battery Independence

A supply chain starts with raw materials, and the U.S. has the resources necessary to build its own battery supply chain. This would help the country avoid supply disruptions like those seen during the oil crises in the 1970s. Battery metals are becoming the new oil and supply chains the new pipelines. It is still early in this new energy era, and the victors are yet to be determined in the battery arms race. on Did you know that nearly one-fifth of all the gold ever mined is held by central banks? Besides investors and jewelry consumers, central banks are a major source of gold demand. In fact, in 2022, central banks snapped up gold at the fastest pace since 1967. However, the record gold purchases of 2022 are in stark contrast to the 1990s and early 2000s, when central banks were net sellers of gold. The above infographic uses data from the World Gold Council to show 30 years of central bank gold demand, highlighting how official attitudes toward gold have changed in the last 30 years.

Why Do Central Banks Buy Gold?

Gold plays an important role in the financial reserves of numerous nations. Here are three of the reasons why central banks hold gold:

Balancing foreign exchange reserves Central banks have long held gold as part of their reserves to manage risk from currency holdings and to promote stability during economic turmoil. Hedging against fiat currencies Gold offers a hedge against the eroding purchasing power of currencies (mainly the U.S. dollar) due to inflation. Diversifying portfolios Gold has an inverse correlation with the U.S. dollar. When the dollar falls in value, gold prices tend to rise, protecting central banks from volatility. The Switch from Selling to Buying In the 1990s and early 2000s, central banks were net sellers of gold. There were several reasons behind the selling, including good macroeconomic conditions and a downward trend in gold prices. Due to strong economic growth, gold’s safe-haven properties were less valuable, and low returns made it unattractive as an investment. Central bank attitudes toward gold started changing following the 1997 Asian financial crisis and then later, the 2007–08 financial crisis. Since 2010, central banks have been net buyers of gold on an annual basis. Here’s a look at the 10 largest official buyers of gold from the end of 1999 to end of 2021: Rank CountryAmount of Gold Bought (tonnes)% of All Buying #1🇷🇺 Russia 1,88828% #2🇨🇳 China 1,55223% #3🇹🇷 Türkiye 5418% #4🇮🇳 India 3956% #5🇰🇿 Kazakhstan 3455% #6🇺🇿 Uzbekistan 3115% #7🇸🇦 Saudi Arabia 1803% #8🇹🇭 Thailand 1682% #9🇵🇱 Poland1282% #10🇲🇽 Mexico 1152% Total5,62384% Source: IMF The top 10 official buyers of gold between end-1999 and end-2021 represent 84% of all the gold bought by central banks during this period. Russia and China—arguably the United States’ top geopolitical rivals—have been the largest gold buyers over the last two decades. Russia, in particular, accelerated its gold purchases after being hit by Western sanctions following its annexation of Crimea in 2014. Interestingly, the majority of nations on the above list are emerging economies. These countries have likely been stockpiling gold to hedge against financial and geopolitical risks affecting currencies, primarily the U.S. dollar. Meanwhile, European nations including Switzerland, France, Netherlands, and the UK were the largest sellers of gold between 1999 and 2021, under the Central Bank Gold Agreement (CBGA) framework. Which Central Banks Bought Gold in 2022? In 2022, central banks bought a record 1,136 tonnes of gold, worth around $70 billion. Country2022 Gold Purchases (tonnes)% of Total 🇹🇷 Türkiye14813% 🇨🇳 China 625% 🇪🇬 Egypt 474% 🇶🇦 Qatar333% 🇮🇶 Iraq 343% 🇮🇳 India 333% 🇦🇪 UAE 252% 🇰🇬 Kyrgyzstan 61% 🇹🇯 Tajikistan 40.4% 🇪🇨 Ecuador 30.3% 🌍 Unreported 74165% Total1,136100% Türkiye, experiencing 86% year-over-year inflation as of October 2022, was the largest buyer, adding 148 tonnes to its reserves. China continued its gold-buying spree with 62 tonnes added in the months of November and December, amid rising geopolitical tensions with the United States. Overall, emerging markets continued the trend that started in the 2000s, accounting for the bulk of gold purchases. Meanwhile, a significant two-thirds, or 741 tonnes of official gold purchases were unreported in 2022. According to analysts, unreported gold purchases are likely to have come from countries like China and Russia, who are looking to de-dollarize global trade to circumvent Western sanctions.

There were several reasons behind the selling, including good macroeconomic conditions and a downward trend in gold prices. Due to strong economic growth, gold’s safe-haven properties were less valuable, and low returns made it unattractive as an investment.

Central bank attitudes toward gold started changing following the 1997 Asian financial crisis and then later, the 2007–08 financial crisis. Since 2010, central banks have been net buyers of gold on an annual basis.

Here’s a look at the 10 largest official buyers of gold from the end of 1999 to end of 2021:

Source: IMF

The top 10 official buyers of gold between end-1999 and end-2021 represent 84% of all the gold bought by central banks during this period.

Russia and China—arguably the United States’ top geopolitical rivals—have been the largest gold buyers over the last two decades. Russia, in particular, accelerated its gold purchases after being hit by Western sanctions following its annexation of Crimea in 2014.

Interestingly, the majority of nations on the above list are emerging economies. These countries have likely been stockpiling gold to hedge against financial and geopolitical risks affecting currencies, primarily the U.S. dollar.

Meanwhile, European nations including Switzerland, France, Netherlands, and the UK were the largest sellers of gold between 1999 and 2021, under the Central Bank Gold Agreement (CBGA) framework.

Which Central Banks Bought Gold in 2022?

In 2022, central banks bought a record 1,136 tonnes of gold, worth around $70 billion. Türkiye, experiencing 86% year-over-year inflation as of October 2022, was the largest buyer, adding 148 tonnes to its reserves. China continued its gold-buying spree with 62 tonnes added in the months of November and December, amid rising geopolitical tensions with the United States. Overall, emerging markets continued the trend that started in the 2000s, accounting for the bulk of gold purchases. Meanwhile, a significant two-thirds, or 741 tonnes of official gold purchases were unreported in 2022. According to analysts, unreported gold purchases are likely to have come from countries like China and Russia, who are looking to de-dollarize global trade to circumvent Western sanctions.